The GENIUS Act framework explained

The GENIUS Act, signed into law on July 18, 2025, establishes the first comprehensive federal regulatory framework for payment stablecoins in the United States. The legislation directs the Department of the Treasury to issue implementing regulations that define which entities may issue stablecoins and mandate strict reserve requirements to ensure stability. This federal preemption standardizes oversight, replacing the fragmented patchwork of state-level money transmitter laws that previously governed the industry.

Under the new framework, only federally chartered banks, thrift institutions, or payment stablecoin issuers registered with the OCC are permitted to issue regulated stablecoins. The Office of the Comptroller of the Currency (OCC) has issued a Notice of Proposed Rulemaking (NPR) to operationalize these provisions, focusing on reserve asset composition, redemption rights, and anti-money laundering (AML) compliance. Issuers must hold reserves in cash and short-term U.S. government obligations, ensuring that stablecoins remain redeemable at par value at all times.

This regulatory structure aims to mitigate systemic risk by treating stablecoins similarly to traditional money market funds or bank deposits in terms of reserve safety. By centralizing oversight under federal authorities, the GENIUS Act seeks to protect consumers while fostering innovation in digital asset payments. The Treasury and OCC continue to refine these rules through public comment periods, with final regulations expected to take full effect in 2026.

Market share shifts between USDC and USDT

The GENIUS Act establishes a distinct regulatory hierarchy that favors issuers operating under direct federal supervision. This legal framework creates a structural advantage for USD Coin (USDC) over Tether (USDT), as USDC is issued by Circle, an entity that has actively sought compliance with the new federal standards. Tether, by contrast, operates primarily under offshore structures and lacks the same level of integration with US banking regulators.

Regulatory capital requirements under the GENIUS Act impose strict reserve audits and liquidity mandates. These requirements increase operational costs for stablecoin issuers, effectively raising the barrier to entry. Established US-based issuers like Circle are positioned to absorb these costs more efficiently than offshore competitors. This dynamic is already visible in institutional adoption trends, where corporate treasuries prioritize issuers with clear US regulatory oversight to mitigate counterparty risk.

The competitive landscape is shifting as institutional capital flows toward compliant assets. While USDT retains significant retail market share, USDC is capturing a disproportionate share of new institutional volume. This divergence highlights the market's response to regulatory clarity, with compliance becoming a primary driver of asset preference rather than mere price stability.

| Issuer | Regulatory Status | Reserve Audit Frequency | Institutional Preference |

|---|---|---|---|

| USDC (Circle) | OCC-regulated bank partner | Monthly third-party attestation | High |

| USDT (Tether) | Offshore entity (BVI) | Quarterly limited assurance | Moderate |

CBDCs versus private stablecoins

The GENIUS Act, enacted in July 2025, explicitly distinguishes private payment stablecoins from central bank digital currencies (CBDCs). While both serve as digital mediums of exchange, their legal foundations and operational structures differ fundamentally. Private stablecoins are issued by regulated financial institutions—such as banks and credit unions—backed by reserves of high-quality liquid assets. In contrast, a CBDC would represent a direct liability of the central bank, altering the traditional banking relationship between the state and the individual.

This distinction matters for monetary policy and financial stability. The Federal Reserve has noted that payment stablecoins offer efficiency gains in cross-border payments without replacing the dollar’s role. A CBDC, however, could bypass commercial banks by allowing citizens to hold accounts directly with the Federal Reserve. The GENIUS Act does not authorize a U.S. CBDC; it focuses exclusively on regulating private issuance. This separation ensures that the private sector drives innovation in digital payments while the government retains control over monetary issuance.

The regulatory framework treats these two systems as parallel but distinct. Private stablecoins must maintain full reserve backing and undergo regular audits to protect consumers. CBDCs remain a theoretical policy option, with no legislative path forward in the current Congress. Understanding this boundary clarifies why the GENIUS Act targets private issuers rather than central bank currency.

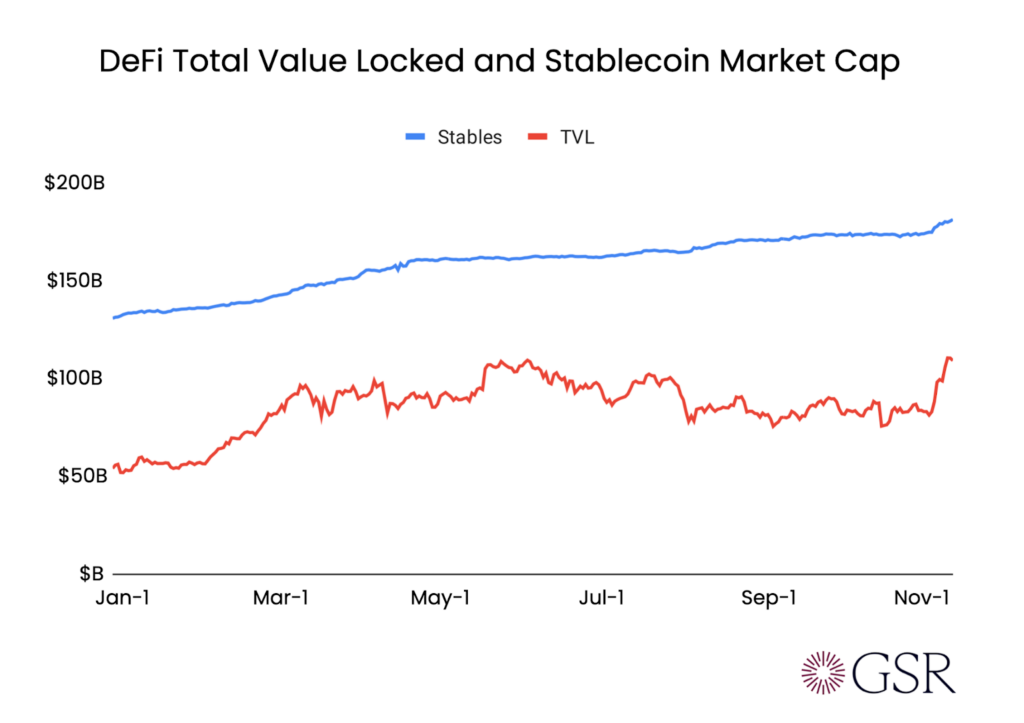

Stablecoin reserves and real-world asset tokenization

The GENIUS Act mandates that stablecoin issuers hold reserves in highly liquid, low-risk assets. This requirement is driving a structural shift from traditional bank deposits toward tokenized Real-World Assets (RWA). By converting government securities and short-term debt into on-chain instruments, issuers can satisfy regulatory liquidity standards while maintaining transparent, real-time proof of reserves.

Tokenization allows these reserve assets to be programmatically verified. Instead of relying on periodic bank statements, issuers can provide cryptographic proof that the underlying assets exist and are segregated from corporate balance sheets. This transparency reduces counterparty risk and aligns with the Federal Reserve’s broader interest in digital settlement layers.

The shift also impacts yield generation. Historically, stablecoin issuers earned interest from cash deposits at commercial banks. Under the new framework, issuers are increasingly turning to tokenized Treasury bills and commercial paper. This transition supports demand for US debt while ensuring that reserve assets remain compliant with the strict liquidity requirements outlined in the proposed rules.

Compliance checklist for issuers

Issuers must align their operational and reporting structures with the framework established by the GENIUS Act. The following steps outline the core requirements for maintaining compliance in 2026.

Payment stablecoin issuers must register directly with the Federal Reserve. This registration is mandatory for any entity issuing stablecoins intended for general payment purposes, regardless of whether they operate as a bank or non-bank entity.

Issuers must hold fully reserved assets in segregated accounts. The GENIUS Act requires these reserves to be held in cash or cash equivalents, ensuring that every token in circulation is backed by a corresponding liquid asset available for redemption on demand.

Treasury proposals require robust anti-money laundering (AML) and sanctions compliance frameworks. Issuers must screen transactions against OFAC lists and maintain detailed records of user identity to prevent illicit financial flows through stablecoin networks.

Issuers must provide quarterly attestation reports from an independent public accountant. These reports verify the sufficiency and quality of the reserve assets, ensuring that the issuer maintains the required 1:1 backing ratio at all times.

Non-bank issuers with less than $10 billion in outstanding stablecoins may opt for state-level regulation. This option provides a streamlined path to compliance, provided the issuer meets specific capital and reporting standards set by their home state regulator.

Compliance is not optional. Issuers who fail to meet these standards face significant penalties, including forced redemption of tokens and potential criminal liability for willful violations.

No comments yet. Be the first to share your thoughts!